Appraisers use three different methods to estimate the value of a property. The income approach considers the value as the present value of future expected cash flows generated by the property. It is most accurate when valuing commercial properties with rental income in active markets. The sales comparison method relates the estimated value of the subject property to similar properties that have recently sold in the same market. This method is particularly useful when the comparable properties and the subject property are highly similar and were sold within the past few months. That means the sales comparison method also relies on an active market for similar properties.

On the other hand, the cost approach to valuation is the one method that is not dependent upon an active market for similar properties. Instead, the cost approach estimates the property value as the value of its components, the underlying land, and the depreciated value of the improvements. In this article, we’ll take a deep dive into how the cost approach to valuations works.

Although the details are more complicated, the basic formula for valuing a property using the cost approach is:

The cost approach is based on the economic belief that informed buyers will not pay any more for a product than they would for the cost of producing a similar product that has the same level of utility. The cost approach to valuation is easy to use when the property is new and represents the highest and best use of the property. In this case, cost new is known because the improvements were just built. In addition, there should be a negligible amount of accumulated depreciation. Since the cost approach does not rely on comparables, it is also useful when valuing a special use property or a property with unique components.

Cost new can be defined in two different ways. Replacement cost new is the current cost to construct a building with the same utility using the current construction materials while adhering to current standards, designs, and layouts. Reproduction cost new is the current cost to construct an exact duplicate of the property with the same materials and construction practices according to the design, layout, and standards in place at the time the property was initially constructed. For relatively new properties, there is virtually no difference in replacement cost and reproduction cost. The more unique or historic a property is, however, the bigger the cost difference between reproduction and replacement cost. Building an exact replica of a historic home is much more expensive than building a new home.

When considering the costs of construction, it is important to consider both direct costs and indirect costs. Direct costs include the materials and labor costs associated with the construction. Indirect costs include costs such as taxes, administrative fees, financing costs, professional fees, and insurance. There are four main methods to estimate cost new when calculating either replacement cost or reproduction cost.

Depreciation causes the difference in value between the cost new of the improvements and the current contributing value of the improvements. The three forms of depreciation are physical, functional, and external depreciation. Physical depreciation results from normal wear and tear on the property that happens with age. Functional depreciation is the result of changes in needs or preferences over time that cause a reduction in the property’s utility. External depreciation is the result of adverse neighborhood or economic trends. There are three methods that appraisers can use to estimate depreciation.

There are many techniques that appraisers can use to estimate land value, but all of them are essentially some form of the income approach or the sales comparison approach. Direct comparison is the most common method for estimating land value. The price of land is simply derived from recently sold plots of land. It can also be computed as a residual value using the cost approach equation for a newly constructed property, where the cost new and sales price are both known.

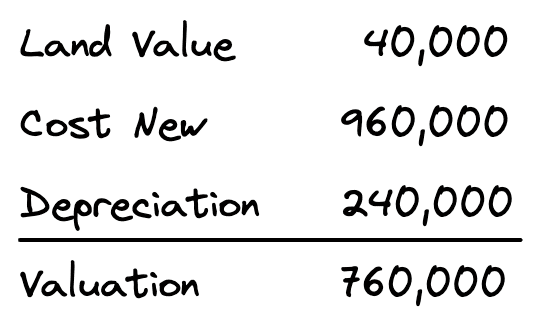

Suppose an appraiser is using the cost approach to estimate the value of a property on 1 acre of land. Sites of similar size and location sell for around $40,000. Using the comparative unit method, an appraiser finds that the cost new for a building of similar construction materials and quality is $40/sqft for a 24,000-sqft building. So, the cost new of the improvements is $960,000. The improvements have an estimated total economic life of 40 years and a remaining economic life of 30 years. The age-life method of depreciation suggests that the improvements should be depreciated by 25% since they have aged the equivalent of 10 out of 40 years. The appropriate depreciation deduction is 25% of the $960,000, which is $240,000. Using the cost approach, the appraiser estimates the final property value is $760,000.

In this article, we discussed the cost approach to valuation, which is commonly used by commercial real estate appraisers. We compared the cost approach vs the sales comparable approach and also the cost approach vs the income approach. The primary difference with the cost approach is that it does not require an active market. The cost approach determines value by adding the value of the land to the cost of a new equivalent building, then subtracting out any depreciation. We walked through how appraisers calculate cost new, depreciation, and also how land value is determined. Finally, we went through a cost approach example step by step to show how the cost approach can be used to determine property value.